Lihat juga

21.01.2026 12:32 AM

21.01.2026 12:32 AM

If the question is answered briefly, decline only further. Recall that in the first half of last year, the main downward factor for the US currency was the trade war Donald Trump launched worldwide. Even the monetary policy of the Federal Reserve, the European Central Bank, and the Bank of England played only a background role for market participants. Otherwise, in the first half of 2025, the euro would not have risen almost 15% against the dollar. At that time, the ECB was actively cutting interest rates.

In the second half of last year, the market grew tired of selling the dollar and took a pause that continues to this day. However, the number of world events that require market reaction has not diminished. Recall that in September, the Fed resumed easing monetary policy, in October, the US experienced a record-long shutdown, and in October, Donald Trump announced new trade tariffs. Thus, even in the second half of last year, market participants had every reason to continue selling the dollar. By the way, at that time, the ECB was already keeping rates unchanged.

The new year began with a positive mood for the US currency. Despite the poor state of the US labour market, demand for the dollar had been slowly growing in recent weeks. However, Trump started the new year as befits a leader of the whole planet. First, the capture of Nicolas Maduro, the president of Venezuela, and then Trump threatened military interventions against practically all Latin American countries. Afterwards, it came to Greenland, which Trump wanted to acquire last year. Nobody intends to give Greenland to Trump "for free," and this time Europeans have the opportunity to respond to the American president from a position of strength. Moreover, Trump himself decided once again to put his cards on the table and exploit other states' dependence on the American market. He imposed an additional 10% tariffs on a number of European countries.

The EU has so far paused to think, since any decision must be approved by the European Parliament and the European Commission. And all of that is very slow. However, if the tariffs do indeed come into effect on February 1, Brussels will have no choice but to respond with its own tariffs or other restrictions on America and its companies. In that case, a new round of trade confrontation will begin, hurting both Europe and the United States—and also the dollar.

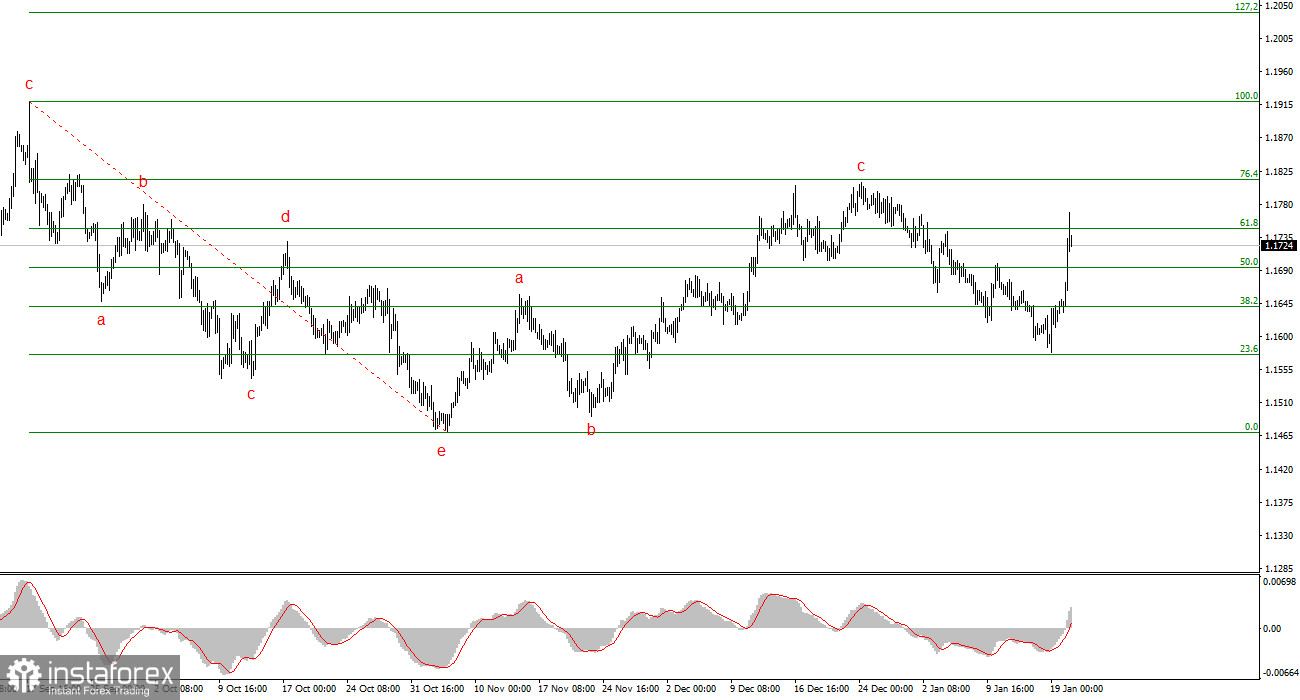

Based on the analysis of EUR/USD, I conclude that the instrument continues to build an upward section of the trend. Donald Trump's policy and the Fed's monetary stance remain significant factors for the long-term decline of the US dollar. Targets for the current trend section may extend to the 25th figure. However, to reach those targets, the market must complete the construction of an extended wave 4. Right now, we only see the market's desire to keep that wave going. Therefore, in the near term, a decline to the 15th figure can be expected.

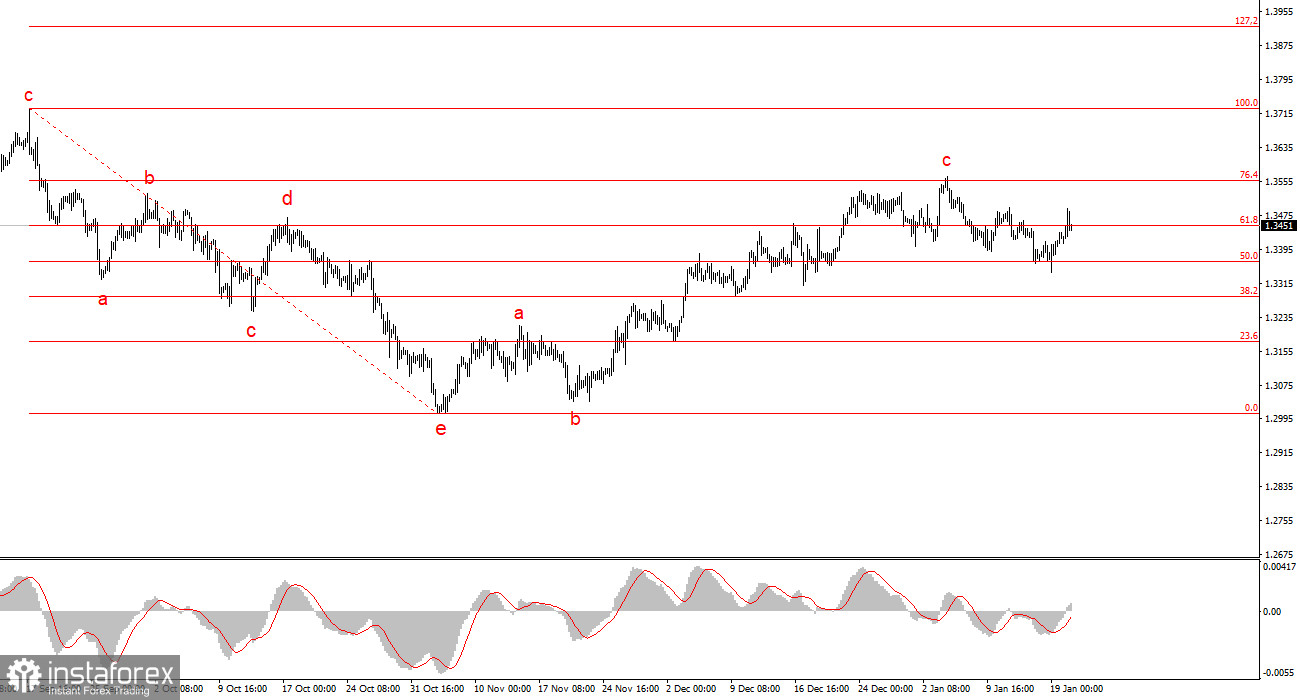

The wave picture for GBP/USD has changed. The downward corrective structure a-b-c-d-e in C within wave 4 appears complete, as does wave 4 itself. If this is indeed the case, I expect the main trend section to resume with initial targets around the 38 and 40 figures.

In the short term, I expected wave 3 or c to form, with targets around 1.3280 and 1.3360, which correspond to 76.4% and 61.8% of Fibonacci. These targets have been reached. Wave 3 or c has presumably completed, so in the near term, a downward wave or a sequence of waves may form.