Lihat juga

24.03.2026 02:03 PM

24.03.2026 02:03 PMIt is generally understood that as long as energy prices remain high, the disinflation process in the UK cannot take hold. If the Monetary Policy Committee previously expected inflation to fall to 2.1% in Q2, it now sees it at about 3%, and therefore, there is no chance of a rate cut.

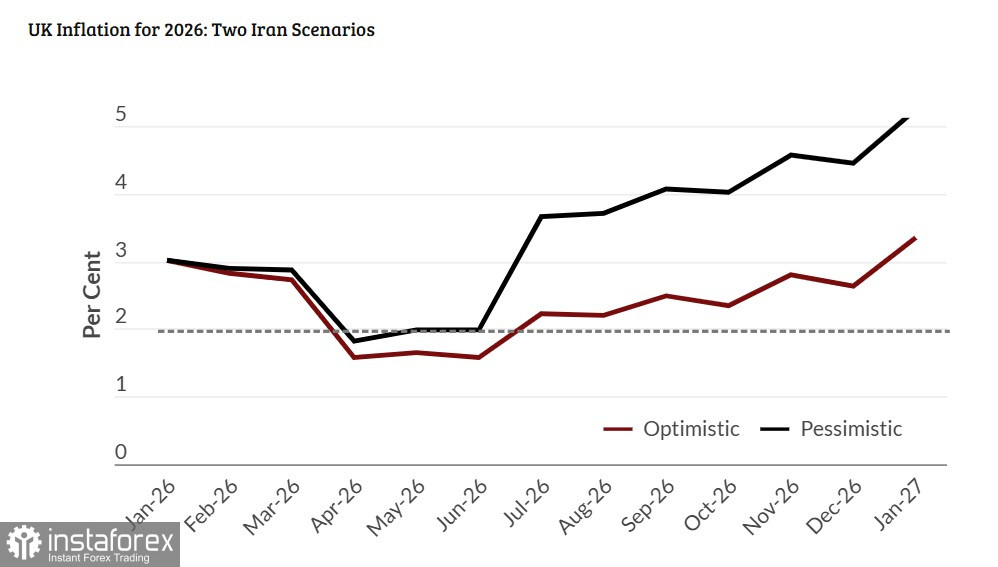

NIESR sees two inflation scenarios depending on how events in the Middle East unfold.

Accoreding to a pessimistic scenario, oil and gas infrastructure in the Persian Gulf and Iran could be largely destroyed, oil prices could reach $200 per barrel or higher, and the crisis effects could persist for several years. In an optimistic scenario, escalation will be contained, prices could stabilize around $120, and it would take several months to replenish global stocks.

In both scenarios, inflation will rise, only at different speeds. From July, this rise will be sustained, and depending on which scenario plays out, it will range from 3% to 5%. NIESR also notes that even the pessimistic scenario could prove optimistic if global escalation occurs and numerous secondary factors, directly or indirectly resulting from sustained higher energy prices, come into play.

So far, the situation is developing more along pessimistic lines. Although yesterday, US President Trump calmed markets by postponing strikes on Iran's energy system due to what he called "very good productive talks," nothing has fundamentally changed, because Iran, according to its officials, is not conducting any talks, and Trump cancelled the strikes under pressure from Iran, which promised responses unacceptable to the US and its allies. If this is the case, the US is further, not closer, to ending the war on its terms, which in any case does not fit the optimistic scenario.

Tomorrow, the UK inflation report for February will be published, which is already outdated, since it does not yet reflect the effects of the war. Economic news is secondary; we proceed from the assumption that there are no reasons for sterling to strengthen, because even higher inflation and a likely tightening by the Bank of England will not outweigh the global consequences of disruption to the world energy system.

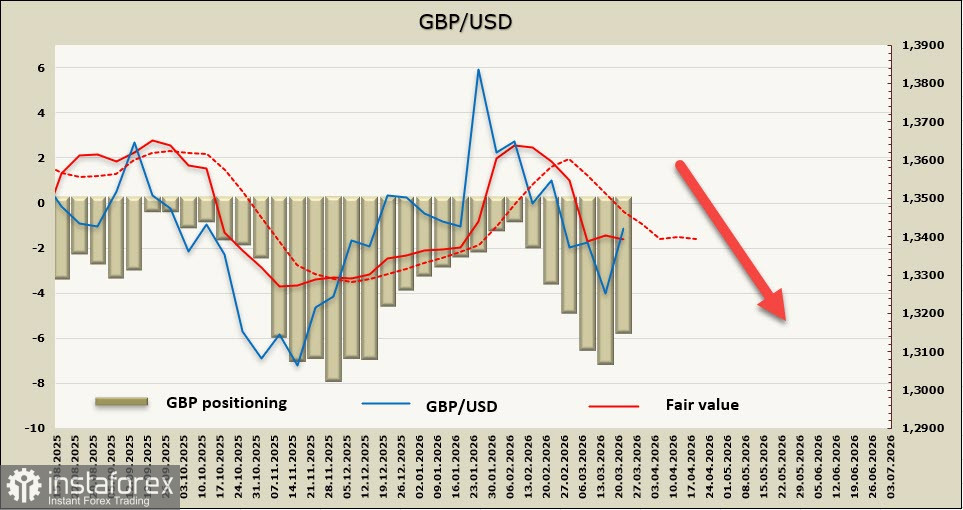

The net short position on GBP decreased over the reporting week by 1.6 billion, to -5.5 billion. Speculative positioning remains bearish, the implied price is below the long-term average, and there are no signs of a reversal yet.

In the previous review, we suggested that the pound, after a brief stabilization, would head down toward support at 1.3000/50. This scenario remains relevant, despite a small pullback after Trump's attempt to defuse escalation. Resistance at 1.3470/90 is unlikely to be breached; attempts to rise can be used as an opportunity to add to new short sales.